Fiscal Policy

Contents

- The Spanish Budgetary System

- Fiscal Policy Objectives and Macroeconomic Environment

- Fiscal Policy in 2015

- The Path to Fiscal Consolidation

- The budget year 2015

- Tax reform

- Impact of legal changes in 2015

- Second Chance

- National Budget for 2016

- Links

The Spanish budgetary system

In the financial sphere, Spain's administrative decentralization into three levels of government (central, regional and local) is guided by the principles of financial autonomy, coordination and solidarity, as enshrined in the Spanish Constitution of 1978.

The autonomous communities and local authorities enjoy full financial autonomy to adopt and manage their own budgets.

At the national level, the drafting of the Central Government budget rests with the Central Government, and the scrutiny, amendment and adoption of the Budget lies within the purview of the Cortes Generales, the Spanish national parliament.

The Central Government Budget (Spanish "PGE") is the document setting out the annual plan of revenue and expenditure commitments for the central public sector. The Central Government Budget is one of the Government's key instruments of economic policy, specifying the strategic goals of the various public policies and the funds appropriated to pursuing them.

The legal framework of the Central Government Budget is mostly provided by three enactments: the Spanish Constitution, which devotes Article 134 to the Central Government Budget; the Budgetary Statute Law of 2003 (Ley 47/2003), and the Budgetary Stability and Financial Sustainability Statute Law of 2012 (Ley Orgánica 2/2012).

Fiscal policy objectives and macroeconomic environment

The Spanish economy first set out on the path to economic recovery in the third quarter of 2013, bringing an end to what was a deep and prolonged recession. The reasons for this favourable economic development lie in the economic policy implemented by the government since the end of 2011, focusing on two fundamental and interrelated areas: fiscal consolidation and structural reforms.

Reunión del Consejo de Política Fiscal y Financiera (Ministerio de Hacienda y Función Pública)From the very start of the government's term of office, fiscal policy has been geared towards putting public finances back on a path of fiscal stability and financial sustainability. This is an essential element for achieving sustainable growth and promoting job creation, while maintaining the system of social protection and paying particular attention to correcting inequalities.

Reunión del Consejo de Política Fiscal y Financiera (Ministerio de Hacienda y Función Pública)From the very start of the government's term of office, fiscal policy has been geared towards putting public finances back on a path of fiscal stability and financial sustainability. This is an essential element for achieving sustainable growth and promoting job creation, while maintaining the system of social protection and paying particular attention to correcting inequalities.

Reducing the deficit of 8.9% in 2011 to 6.3% in 2013, thus meeting the target set by the EU, was achieved under highly adverse cyclical conditions that involved a contraction of the tax base with a consequent reduction in government revenues and the inevitable increase in certain items in expenditure items, such as unemployment benefits and servicing debt. The consolidation effort has been the biggest among the G-20 countries. While the fiscal policy followed has meant that the domestic economic context for the 2015 General State Budget is more favourable than in previous years, progress must continue to be made on fiscal consolidation and on boosting economic growth, with particular focus on job creation.

The goal of fiscal policy is therefore to achieve the correct balance of income and expenditure capable of promoting growth, while maintaining the system of social protection and tackling the inequalities generated by the crisis. This is the general thrust of the tax reform, which will serve to reduce the tax burden on employment income, increase consumption and investment, promote the capitalisation of companies and improve the economy's competitiveness. On the expenditure side, the General State Budget for 2015 increases the efficiency of public spending by aligning it with the new financial framework 2014-2020 of the European Union's budget. This will mean that investment will be programmed and implemented by maximising the use of EU funds and applying the new funding mechanisms available in this new period (such as the use of financial instruments) and through increased participation from the private sector.

The economic background of the General State Budget for 2015 is characterised by the steady recovery of the Spanish economy, which began in the third quarter of 2013. According to advance data from the National Institute of Statistics, the fourth quarter of 2014 posted positive quarterly growth for the sixth consecutive quarter. It has now gathered pace steadily to a rate of 0.7%. In annual terms, the growth rate in the fourth quarter was 2%. This gives a GDP growth rate of 1.4% for 2014 as a whole, twice the figure forecast in the General State Budget for 2014 and 0.1 percentage points (pp) more than forecast in the General State Budget for 2015.

The Spanish economy's recovery has taken place against a backdrop of increasing stability in the financial markets, which has led to a sharp decline in risk premiums and stock market gains, despite stagnation in the Eurozone. This progress in the Spanish economy is driven by stronger domestic demand, which in the fourth quarter of 2014 contributed 2.7 pp to annual GDP growth, thanks to the positive performance of all its components.

However, the contribution of foreign demand has become negative (-0.7 pp) as a result of the recovery process, in which investment has become more significant. Imports have increased, largely due to investment in capital goods (up 10.4% in 3Q14 compared with -31.1% in 2Q09). This demonstrates the boost that our companies have chosen to give to investment on the back of the confidence that now exists in Spain's recovery. Economic logic has thus inevitably brought us an increase in private consumption and job creation. The Spanish economy has obtained consecutive surpluses in its non-energy trade balance since 2012, which had not been seen since 1985. In this context, Spain continues to be capable of attracting foreign finance.

The competitiveness of the Spanish economy has been improving significantly. While unit labour costs in Spain grew at rates in excess of 3% until 2009, they began to fall at rates of around 3% as from 2012. As a result of this process of internal devaluation, Spain has been at the forefront of the EU in terms of gains in competitiveness: whereas labour costs rose by 4.5% in the Eurozone (base of 100 in 2010), since 2009 the trend for the Spanish economy has been in the opposite direction, with costs falling by 6.9%.

Inflation also began to trend down as from 2013, which in general has continued into 2014, with the inflation rate for the year standing at -0.2%, compared with the figure for the Eurozone of 0.4%.

It is important to highlight the achievement of the Spanish economy in moving from a borrowing requirement from the rest of the world, which was up to around 10% of GDP in 2007, to a net lending capacity in 2014 of 0.5% of GDP, meaning that any new financing needs are covered by the country's own resources.

Fiscal policy in 2015

Fiscal policy since the start of this government's term of office is playing a decisive role in the exit from the crisis. The transfer of monetary policy to the European Central Bank restricted Spain's use of economic policy instruments to tackle a crisis of international scope, which was especially severe in our country, so that fiscal policy assumed a greater role than in previous recessions.

To this we must add that the sharp deterioration in Spain's public finances in the early years of the crisis required the application of a firm policy of fiscal consolidation, in order to return to a sustainable path and restore credibility to the Spanish economy. Spain's position deteriorated from a surplus of 2% of GDP in 2007 to a deficit of 11% in 2009. The fiscal position of all the Eurozone countries worsened over this period, but in the case of Spain this phenomenon was quantitatively far greater, to the extent that the situation of public finances was perceived as one of the major risk factors for our economy.

Emblema de la Real Casa de la Moneda (Ministerio de la Presidencia y para las Administraciones Territoriales)In this context, the present government reacted by applying an unprecedented fiscal correction to ensure solvency and restore confidence in the Spanish economy in the fragile financial environment of the Eurozone. This necessary fiscal consolidation and an array of ambitious structural reforms are the two pillars of economic policy applied from the start of the government's term of office. They are already bearing fruit.

Emblema de la Real Casa de la Moneda (Ministerio de la Presidencia y para las Administraciones Territoriales)In this context, the present government reacted by applying an unprecedented fiscal correction to ensure solvency and restore confidence in the Spanish economy in the fragile financial environment of the Eurozone. This necessary fiscal consolidation and an array of ambitious structural reforms are the two pillars of economic policy applied from the start of the government's term of office. They are already bearing fruit.

Sticking to fiscal policy, government action has not only focused on controlling the deficit; it has undertaken a comprehensive reform of the legal framework to ensure fiscal discipline at all levels of government and to ensure the sustainability of the welfare system.

The Constitutional Law on Budgetary Stability and Financial Sustainability, the launch of the Independent Fiscal Responsibility Authority, the raft of measures to combat late payments to businesses by public authorities and the recent creation of the Economic and Financial Information Centre have all significantly improved fiscal governance rules for the Public Administration, institutionalising fiscal discipline and the transparency of financial information. There have also been major reforms to bolster the welfare state, for example, the review of the pension system or streamlining measures that ensure the viability and quality of basic public services. At the same time as the reform of the framework of tax governance, the government has implemented an effective policy of consolidating public finances to reduce unsustainable levels of public debt, combining cost reduction with measures to increase revenues.

The strategy of deficit reduction is asymmetric in nature, since the adjustment involves a bias towards measures that reduce public spending. Naturally this fiscal effort is shared by all public administration services, as Spain is the OECD country with the most decentralised spending (approximately 45% of total expenditure is administered by local or regional governments). Another feature of the consolidation strategy is its extreme fairness, as the fiscal efforts demanded on the side of both revenues and expenditure are non-linear. As the IMF has acknowledged, Spain has carried out a progressive fiscal consolidation policy, as agents with the biggest economic capacity have assumed the greatest burden. Finally, the structural nature of our consolidation strategy is worth noting, which has been based primarily on measures with a permanent impact on the public accounts.

In the first two years of this fiscal policy, the budget deficit, measured according to the new ESA 2010, has fallen from 9.0% in 2011 to 5.8% by the end of 2014, excluding support to the financial sector. This has been key in recovering credibility for the Spanish economy.

The fiscal correction of 3.2 points of GDP has been achieved against a backdrop of a strong economic downturn, which has forced an increase in unavoidable spending such as unemployment benefits and servicing public debt, which required a major fiscal adjustment. This has demonstrated Spain's capacity to control its public accounts and limit them to sustainable levels. As a result of this effort, for the first time since 2007 it has being posting a primary structural surplus as from 2012. This means that expenses (not including interest payments and the effect of the cycle) have been lower than revenues since 2012, which is necessary to ensure debt sustainability.

It is a joint effort in which all tiers of government have tackled their fiscal commitments, substantially improving their fiscal balances.

While the benefits of fiscal policy were already perceived a year ago, it is now, in a context of an accelerating economic recovery, that they are becoming more evident. The consolidation of public accounts continued in 2015, registering a Public Administration deficit (except Local Authorities) of 3.4% of GDP until October 2015, 0.5 points lower than the same period last year.

The path to fiscal consolidation

The favourable economic environment that is expected to extend into the coming years will allow further consolidation of our public accounts without the need for significant adjustments.

After overcoming an initial phase that has put the public accounts in order, and without abandoning fiscal discipline, fiscal policy has incorporated a combination of measures on the revenue and expenditure front to promote economic growth, while not straying from the path of committed consolidation. This path was initially set in the Excessive Deficit Recommendation for Spain, adopted by the ECOFIN Council in July 2013, according to which the public deficit must be below 3% of GDP in 2016, with an intermediate target of 4.2% in 2015.

Within the horizon of the 2015 stability programme, as broken down per tier of government, the central government deficit will be progressively reduced to 0.3% of GDP by 2018, while the regional governments will balance their budgets in that year.

The budget year 2015

With the data available as at 22 December 2015, in the period January-November the State registered a deficit of 27.52 billion euros in terms of the national accounts, a fall of 22.2% on the figure for the same period in 2014. In terms of GDP, the deficit is equivalent to 2.55%, well below the 3.4% in registered in November 2014.

The primary deficit, which does not include interest on public debt, has declined to 535 million euros (0.05% of GDP, compared with a deficit of 7.63 billion registered the same month last year (0.73% of GDP). The fall of 93% in the primary deficit is a result of the significant decline in the public deficit.

Non-financial State revenues

Non-financial State resources registered year-on-year growth of 4.7% to 163 billion, boosted by the growth of tax revenues, which increased by 6.6%. Taxes on production and imports grew by 7.8%, with VAT revenue particularly good. Current taxes on income and wealth, which includes revenues from Personal Income Tax and Corporate Income Tax, increased by 5% to November, despite the tax cuts introduced in the tax reform.

Presentación del Informe de Expertos sobre la Reforma Fiscal (Ministerio de Hacienda y Función Pública)

Presentación del Informe de Expertos sobre la Reforma Fiscal (Ministerio de Hacienda y Función Pública)Property income fell by 46.7%. As in previous months, this fall is due to two factors: the fall in dividends due to the decline in those corresponding to the Bank of Spain, and the reduced interest income, which fell by 54.5%, as in 2015 an interest rate of 0% was set for all loans to the regional governments and local authorities through extraordinary funding mechanisms.

Non-financial State expenditure

Non-financial State expenditure fell to 190.52 billion, 0.3% down on the period January-November 2014. Not including the partial repayment of the bonus payment for 2012, non-financial expenditure declined by 0.5%.

Intermediate expenditure increased by 7.1% in November due to the increase in expenses for the general elections. There was also an increase in salaried remuneration due to the partial payment of the bonus for 2012 (2.6%) and the social benefits other than social transfers-in-kind resulting from higher retirement pensions, which rose by 3.4%.

Among the items that declined are interest payments, which fell by 2.7% year-on-year, as well as current transfers between the public authorities, which fell by 2.4%. This is basically due to the fall in transfers in Social Security funds as a result of the fall of 30% of those allocated to the State Public Employment Service because of the stronger labour market. In contrast, transfers to regional governments and local authorities have increased by 2.4% and 2% respectively.

Capital consumption includes growth of 8.7% in gross fixed capital formation, as well as an increase in transfers of capital between public authorities of 507 million euros, mainly due to increased transfers to ADIF [Railway Infrastructure Administrator] and IDAE [Institute for Energy Diversification and Savings].

Tax reform

The Spanish economy began its economic growth in 2013, and the trend became consolidated and gathered pace as increased structural reforms and control of the public deficit recovered confidence in the economy and improved its growth prospects.

The consolidation in the economic recovery, together with the great strength shown by tax revenues, led the government to incorporate new measures into the established fiscal policy through a two-stage tax reform, the first entering into force on 1 January 2015 and the second planned for 1 January 2016.

The aims of this reform are clear: to boost economic growth, create jobs and improve business competitiveness through the creation of a fairer tax system that includes a cut in taxes. The tax policy until then had created good conditions, with incipient economic growth, but these had to be underpinned and boosted through a tax reform that could put more money into the hands of households and companies.

Oficinas de la Agencia Tributaria (Ministerio de Hacienda y Función Pública)Only in a context of economic growth, favourable prospects on the future development of the Spanish economy and a recovery of the taxable bases can the tax reform have a significant impact on the real economy, stimulating growth and job creation and thus enabling a net increase in revenues. The tax reform includes a set of measures that reduce the tax burden on 20 million taxpayers, above all those on middle and low incomes, and simplify and modernise the main taxes to encourage savings and investment, boost company competitiveness and economic growth and support the fight against fraud.

Oficinas de la Agencia Tributaria (Ministerio de Hacienda y Función Pública)Only in a context of economic growth, favourable prospects on the future development of the Spanish economy and a recovery of the taxable bases can the tax reform have a significant impact on the real economy, stimulating growth and job creation and thus enabling a net increase in revenues. The tax reform includes a set of measures that reduce the tax burden on 20 million taxpayers, above all those on middle and low incomes, and simplify and modernise the main taxes to encourage savings and investment, boost company competitiveness and economic growth and support the fight against fraud.

With respect to Personal Income Tax, there was a reduction in the number of tax bands and marginal rates applicable to them. The average cut will be 12.5%, with the biggest cut for taxpayers on the lowest income. Around 1.6 million taxpayers will no longer be liable to pay tax. There will also be a general cut in tax withheld on all employees and some self-employed people, which represents a direct injection of liquidity into the real economy. With respect to savings, a cut in its taxation has been included, with a progressive application in the higher bands.

This reform also contains measures designed to increase the fairness of tax that give significant support to the family and other groups that demand special protection, such as the disabled. Family allowances have been increased by up to 32%, and the three "negative taxes" or categories of social benefits have been introduced for large families or families with disabled members.

Corporate Income Tax includes has been cut progressively and measures have been implemented to promote the competitiveness of companies and simplify deductions. The general tax rate has been cut from 30% to 25% in two phases, with the aim of bringing corporate taxation further into line with the rates in other European countries. The tax bases have also been increased to bring the effective rate closer to the nominal rate.

The reform of this tax also includes elements to foster business competitiveness and promote savings and corporate capitalisation. One example is the capitalisation reserve, which replaces the current allowance for profit reinvestment, and represents a cut of 10% in the tax base for increases in equity. In the initial months since the entry into force of the first phase of tax reform its effects on the real economy are already beginning to be seen.

Households are receiving greater disposable income, which is already having an impact in higher consumption. Businesses are increasing fixed capital investment, as well as seeing an improvement in their competitiveness. At the same time, government revenues continue to grow, as do the tax bases of the main taxes. This positive trend, both in the economy and revenues, together with the control maintained over the budget deficit, have allowed the government to anticipate the entry into force of the second phase of the Personal Income Tax reform planned for 2016 to July 2015, through the application of an intermediate rate. The early cut in Personal Income Tax includes not only income from wages, but also from savings. Tax savings have also been favoured by an additional cut through the application of a transitional rate this year.

In the case of the self-employed, the regulation approved extends the reduced withholding rate to all professionals, regardless of their level of income. This measure benefits around 800,000 self-employed, and will inject liquidity of 350 million euros.

In addition, measures have been included to protect the most disadvantaged groups. Thus public financial assistance has been declared exempt from tax in the following cases: for citizens in situations of extreme need or risk of social exclusion; for the food, schooling or other basic needs of minors or people with disabilities; or for victims of violent crime and sexual offences. The possibility of the seizure of certain benefits and financial assistance has also been limited, thus strengthening the protection of the most vulnerable groups. In total, the early introduction of the full Personal Income Tax reform will give back an additional 1,500 million euros to taxpayers, which will improve their disposable income in 2105.

Impact of legal changes in 2015

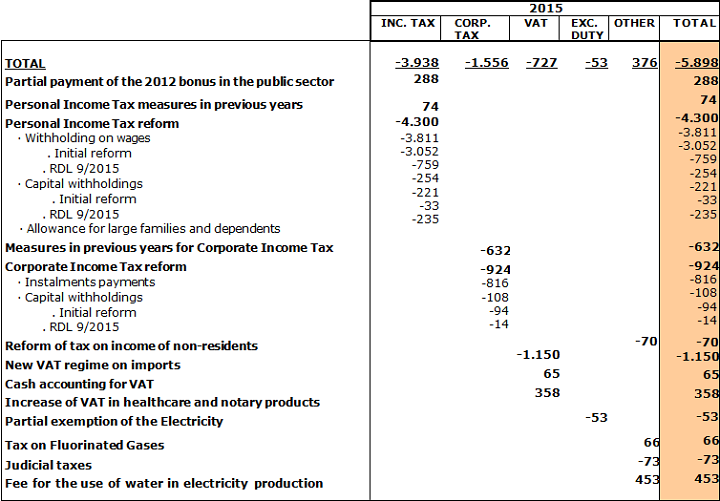

The impact of legal changes from January to November 2015 (information available as at 22 December 2015) amounts to -5.9 billion euros. Table 0 shows the breakdown by figures and measures.

IMPACTS OF THE TAX REFORM IN 2015 (JANUARY-NOVEMBER)

Million euros

Ministry of the Treasury and Public Administration Services

Ministry of the Treasury and Public Administration Services

The reform of direct taxation, both that begun in January and decreed in July, amounted until November to a cost of 5.3 billion euros (4.49 billion of initial measures and 806 million of those that entered into force under Royal Decree-Law 9/2015). The impact of the Personal Income Tax reform was 4.3 billion euros, of which 3.81 billion correspond to tax withholding on wages (3.05 billion under the initial reform and 759 million in July), 235 million of withholding on capital (221 million when the rate was cut from 21% to 20% and 33 million due to the cut to 19.5%) and 254 million to the new allowances introduced earlier than initially planned for large families and dependents. For Corporate Income Tax, the cost is estimated at 924 million euros, 816 million due to the impact of the reform on instalment payments and 108 million due to the fall in the withholding rate on capital income. Finally, in Tax on the Income of Non-Residents (Spanish acronym: IRNR) the cost of the reform is estimated at 70 million euros.

Second Chance

Royal Decree Law 1/2015 of 27 February, was approved by the government with the aim of allowing natural persons who had experienced a business or personal failure to have the possibility to have a fresh start in life and even engage in new enterprises without indefinitely being affected by a debt that they could never have been able to pay off.

A plenary session of the Lower House of Parliament validated the law and also approved its processing as a Bill. Its content was finally enacted as Act 25/2015, of 28 July.

The Preamble to the Royal Decree-Law and the Preamble of the Act state: "Experience has demonstrated that the lack of mechanisms for a second chance creates clear disincentives for undertaking new activities, and even for remaining within the regular circuit of the economy.This is obviously not to the benefit of the debtors themselves, but neither is it to the benefit of creditors, whether public or private. In fact, the mechanisms for a second chance create disincentives for the submerged economy and foster a business culture that will always have a positive impact on employment."

Presentación de los PP. GG. para 2016 (Ministerio de Hacienda y Función Pública)The legal texts are a response to this goal. They regulate various mechanisms that improve the Extra-Judicial Payment Agreement, introduced into the insolvency legislation by Act 14/2013 of 27 September on supporting entrepreneurs and their internationalisation, and introduce an effective mechanism for a second chance for natural persons, aiming to modulate the rigour of the application of Article 1911 of the Civil Code: "Universal asset liability" The debtor's responsibility for his obligations includes all his assets, present and future.

Presentación de los PP. GG. para 2016 (Ministerio de Hacienda y Función Pública)The legal texts are a response to this goal. They regulate various mechanisms that improve the Extra-Judicial Payment Agreement, introduced into the insolvency legislation by Act 14/2013 of 27 September on supporting entrepreneurs and their internationalisation, and introduce an effective mechanism for a second chance for natural persons, aiming to modulate the rigour of the application of Article 1911 of the Civil Code: "Universal asset liability" The debtor's responsibility for his obligations includes all his assets, present and future.

These initiatives allow families and companies to reduce their financial burden, which means additional improvements to those already adopted during this term of office aimed at those who are in a situation close to insolvency due to their economic and social circumstances of vulnerability, whether they are SMEs and self-employed or natural persons in general.

The following have been modified:

- The Insolvency Act 22/2003, aimed at simplifying the use of extra-judicial agreements or regulating the benefit of exoneration of unpaid liabilities when good faith has been demonstrated.

- Royal Decree-Law 6/2012, of 9 March, on urgent measures for mortgage debtors without resources, to increase the threshold of exclusion of debtors of a mortgage-backed loan on their habitual residence.

- The Personal Income Tax Act 35/2006, of 28 November, to declare income that may be declared as a result of repayments and dations in payment of debt exempt from Personal Income Tax, if they have been established by convention, in a legally certified financing agreement or an extra-judicial payment agreement.

In addition to the regulation of the mechanism for a second chance and the improvement of some insolvency institutes, other provisions of a clearly social nature have also been included.

Thus in Title II, together with measures affecting the scope of Social Security (exemptions from contributions to promote the creation of permanent jobs or reductions in contributions for self-employed workers to improve their work/life balance, approval of the reduction from 35 to 20 in the number of day labourers required to access grants for agricultural workers) or the scope of the Administration of Justice (exemptions from certain judicial fees), measures have also been introduced to taxation designed to reduce the tax burden on certain particularly vulnerable groups.

Thus an amendment has been introduced to Act 35/2006, of 28 November on Personal Income Tax and the partial amendment of the laws on Corporate Income Taxes, Income of Non-Residents and on Wealth, with the aim of allowing new groups to apply the allowances included in Article 81 bis of this Law for large families and families who have members with disabilities. The "family cheques" of 1,200 euros per year have been extended to:

- Single parent families with two children.

- Cases where taxpayers are pensioners or receive contributory or welfare benefits from the unemployment protection system.

Act 27/2014, of 27 November on Corporate Income Tax was also amended to exempt partially-exempt enterprises from compliance with formal obligations. An exclusion has been established to the obligation to file a Corporate Income Tax return for enterprises whose total income for the period subject to tax does not exceed a certain amount (a limit of 50,000 euros per year has been established but this was extended to 75,000 euros in the 2016 budget), provided that the total amount of income corresponding to non-exempt income is not greater than 2,000 euros per year, and all the non-exempt income is subject to a withholding.

National Budget for 2016

The draft National Budget for 2016 ratifies the economic policy implemented in recent years and will boost the good results obtained thanks to the measures carried out over these four years. These accounts have therefore been prepared under the same premise of boosting the growth of the Spanish economy and job creation. Compliance with these accounts will maintain the commitment to social spending, which accounts for 53.5%, with an increase of 3.8%.

The budget for 2016 culminates the tax policy developed by the Government since the first and difficult budget drawn up for 2012. These five budgets were each drafted to adapt to the economic reality they were part of, containing the elements needed to emerge from the serious economic crisis that Spain was experiencing. This is the policy with which we have arrived at the current situation, when there is growth at a rate of close to 4% in annualised terms, not counting inflation and with a very positive development of all the variables: consumption, investment, exports and above all job creation. Thus starting in 2106 it is expected that Spain will abandon the Excessive Deficit procedure that it has been implementing since 2009.

Presupuestos Generales de 2015 (Ministerio de Hacienda y Función Pública)Good results of the tax policy applied

Presupuestos Generales de 2015 (Ministerio de Hacienda y Función Pública)Good results of the tax policy applied

This clear improvement in the economic situation is proof that the tax policy of fiscal consolidation and structural reforms implemented since the start has been correct. The budget for 2016 is also in line with the previous budgets and has the main aim of boosting the good results achieved. Its mission will therefore be to consolidate growth and job creation.

The budget, which is based on bringing the tax reform forward that was to enter into force in 2016, involves a significant growth in resources transferred to the territorial public authorities, which will serve to improve benefits in health, education and social services. Thus the funding of the territorial public authorities will increase by 8 billion euros in 2016 (7.8%) on the previous year.

Revenues

Total non-financial revenue for 2016 after the transfer to the territorial bodies will amount to 134.77 billion euros, which represents an increase of 0.8% on the 2015 budget.

Tax income before transfers to the territorial bodies will account for 193.52 billion in 2016, 4% more than in the 2015 budget. By type of tax, income from Personal Income Tax will be 75.43 billion euros, with an increase of 3.4%.

Revenues from Corporate Income Tax will increase by 5.5% to 24.87 billion euros. Income from VAT will grow by 4% to 62.66 billion, while income from Excise Duty will increase by 0.8% to 20.05 billion euros.

Expenditure

The favourable impact of growth and the effect on revenues mean that the expenditure budget reflects the recovery in society. The reduction in unemployment expenditure and the financial burden of the public debt will help increase social expenditure, which has increased by 3.8%.

It is worth highlighting that it is a budget in which fundamental items will be increased, such as those for civil research, funding of the Educational Improvement Act (Spanish acronym: LOMCE), international cooperation, employment promotion, improvement of assistance to families and the system of dependence as well as the special refugee relocation plan.

Public-sector employees

Logo de la Agencia Estatal de Administración Tributaria (Ministerio de Hacienda y Función Pública)

Logo de la Agencia Estatal de Administración Tributaria (Ministerio de Hacienda y Función Pública)

The public accounts for next year also include compliance by the government with its commitment to compensate as far as possible the efforts made by the citizens as a result of the adjustment measures that had to be taken. Public employees, whose contribution was essential for emerging from the crisis, will have their remuneration updated by 1%, following the cut in 2010 and the two years of wage freezes. They will also be paid 50% of the bonus they did not receive in 2012. Similarly, the sixth day off for personal reasons has been restored, together with a further three days depending on seniority. A replacement rate of 100% was established for priority sectors and 50% for the rest.

It is a budget that also continues with the investments for the CRECE Plan, which is trying to align the objectives of the EU funds with the needs for national investment, supporting economic growth as efficiently as possible.

Another feature of the Act is the requirement to issue informative reports that ensure the support actions for SMEs to companies with a technological base and young entrepreneurs are compatible with the finance granted by the European Union for actions of this kind. The aim is to maximise the capacity of the policies implemented to absorb EU funds.

Links

Facade of the Ministry of the Treasury and Public Administration Services